An insider's guide to prolonging the life of your energy project

Areti Ntaradimou

Posted on: 13 March 2023

We asked Arjan Haring, EU Projects Zone Impact Circle member, to help us demystify the investment scene in Europe.

How to make your project 'market fit' and unlock angel investment, crowdfunding or venture capital

We asked Arjan Haring, EU Projects Zone Impact Circle member, to help us demystify the investment scene in Europe. As a partner at Seldon Digital and project manager at Jheronimus Academy of Data Science, he has a clear view of the investment landscape in the European Union.

So, you have your EU funding and you are about to reach the finish line. What’s next? Which financial instruments do we have?

It's a challenge. Let me try to clarify: by collaborating you build a strong consortium of partner organisations that get funded and work together on a great project. But by competing, your unique organisation can win investment to continue your part after the project. The open innovation paradigm - how I understand it - is trying to bridge this gap.

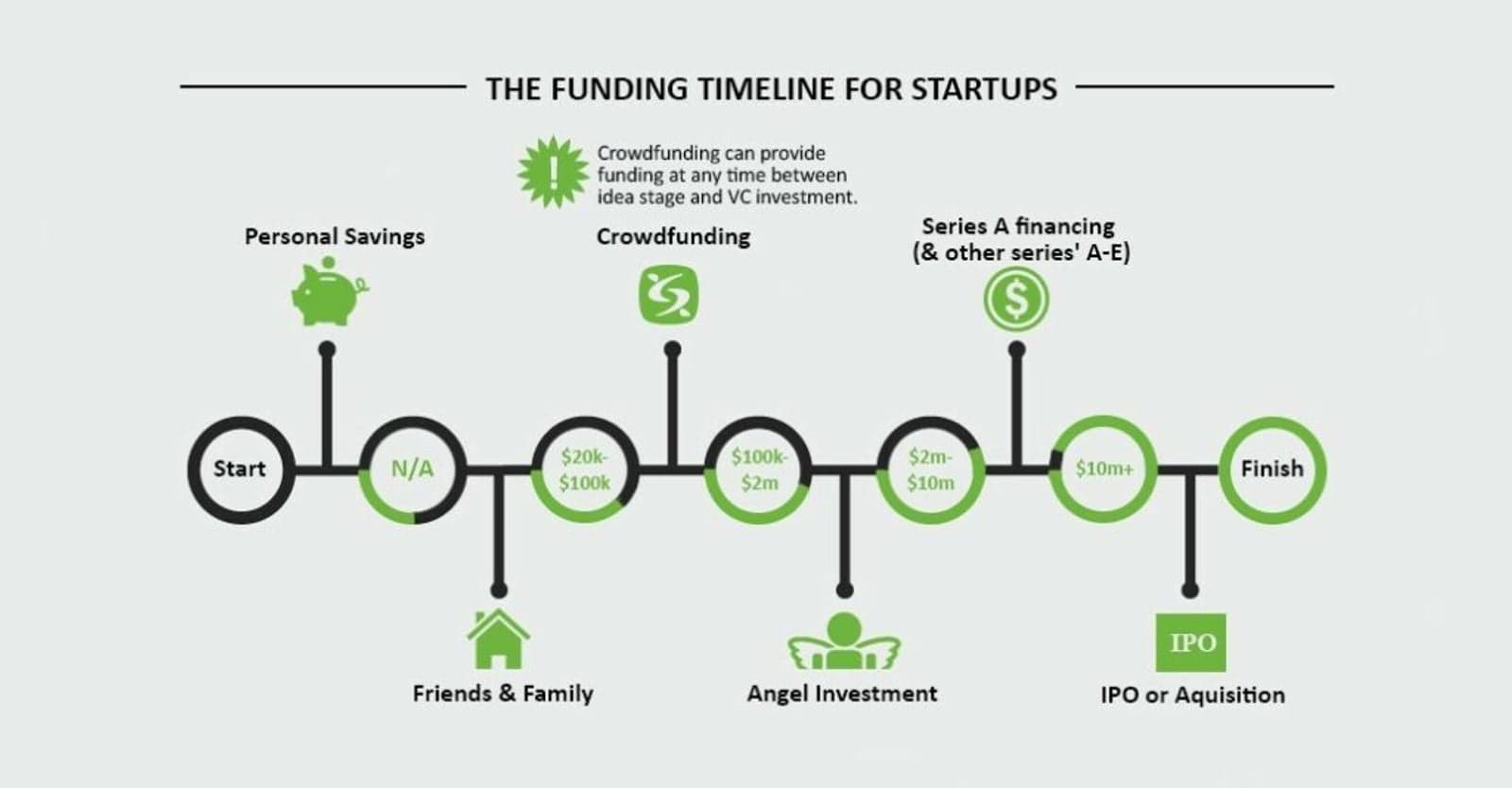

Let's look at the financial instruments individual organizations can choose from. Also, keep in mind: investment is a specific financial instrument that normally works in the context of having some idea that you want to build and get to the market. Here is a helpful figure:

The main funding possibilities are angel investment, crowdfunding and venture capital (series A-E) each at their own specific place along the funding timeline. Although some companies and start-ups that are part of a consortium get investment after the project is finished, we see that this does not happen often.

Coming back to the first point: EU funding is about fostering innovation through collaboration and raising investment is about out-competing other market players. Bridging these worlds potentially unlocks a huge amount of innovation potential.

Which consortiums are more likely to get funding from the EU?

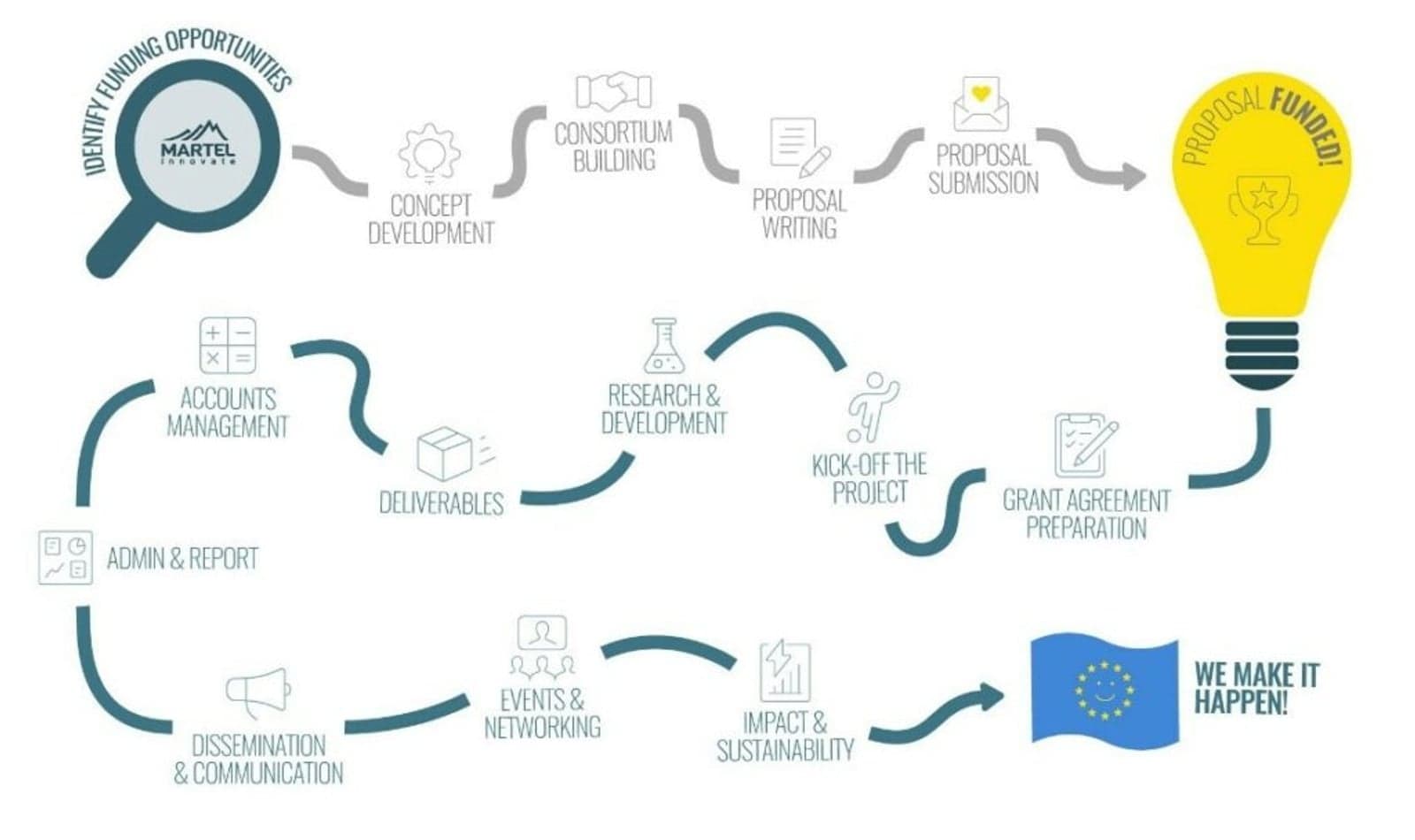

This is less my expertise. But it connects to the former question. Below the traditional route of consortium formation and proposal submission.

I think consortia often have research institutes and universities on board with specific expertise, such as AI, robotics or EV. With international research experts on-board, your proposal is probably more likely to win.

But to link this to the former question: universities work mostly on national and international funding, their relationship with investment is less clear. Sometimes universities can claim intellectual property and shares in a university spin-off (start-up), but normally they require new funding to continue their work.

So, for universities to continue a project, they'll need to start the consortium and proposal process from the start again.

If they want to have an impact with that consortium it could be wise to include a start-up or other organisation that is eligible for investment after the project.

Follow the EU Projects Zone for the latest news about EU Projects

What kind of projects are more likely to get investment?

Projects, or better yet consortia, will not get investment. You need to be a legal entity (for profit or non-profit organisation) to be able to raise investment.

This can also be in the form of a joint-venture where for example two consortium partners continue their collaboration in a newly-founded company.

In addition, a project needs to build something that is of value to the market. An important question to ask yourself as a project lead is whether your project or product is 'market fit'. This means that you have tested whether people want to pay money for your solution. If there is a project market fit, then investors will be more inclined to talk to you.

And finally, another important aspect is how much value the project market fit represents. This means you know the size of your potential market.

Impact investment is a discipline within investment that has grown fast over the last decades. For an impact investor you need to have a good market fit, but also address and have a significant impact on one or more sustainable development goals.

Summarize your panel at Enlit Europe in Frankfurt in 2022 and what is going to be the focus of your sequel panel in Paris in November 2023?

First of all, I want to thank one more time Nuno Brito Jorge, Susana Garayoa, Freerk Bisschop and Philip Lewis for the great discussion we had in Frankfurt. We mostly covered the two different worlds (see fig. 1 and fig. 2) of EU funding and of investment.

We then discussed ways of bridging those worlds. Do you, for example, know that a venture capitalist gets around 3000 pitch decks a year?

A pitch deck is a very succinct way of showing why your idea is worthy of investment. But EU funded project leads often don't know how to make a good pitch deck.

We suggested organising sessions where project leads and investors meet up and discuss how they could better connect.

But the other way around is valuable as well. When investors better know the process of an EU project proposal they know where and when they can help out better.

Investors could, for example, suggest existing start-ups and companies that could add to the strength of a consortium or proposal.

Looking towards the sequel panel discussion in Paris, I believe that we will look at current developments in investment and impact investment specifically.

As well as how that connects to the changing structure of EU project funding. Because one thing is certain, we'll have to keep investing in the innovation power of Europe.

Can you please choose five projects from the EU Projects Zone Directory that, in your opinion, are investment ready?

I would select AI4PV because it has a specific business plan and is a good product market fit. Then, Alva because although it is less product market fit, it is definitely one to watch.

FLEXCoop, because although it is already completed, it has the potential to go further. frESCO, because it is a new take on the already very impactful ESCO formula.

And finally, SocialWatt because it helps bridge the gap between energy companies and social services.