Hedging against renewable volatility with battery storage

Yusuf Latief

Posted on: 3 April 2026

As renewables drive volatility, batteries are emerging as a way to turn that risk into value. Germany and Greece provide interesting case studies.

In this week’s Power Playbook: On paper, BESS are often framed as a flexibility tool; in practice, they start to look a lot more like a hedge.

That distinction matters, particularly as power markets become increasingly shaped by volatility rather than averages.

A recent case study from Statkraft on Germany illustrates why.

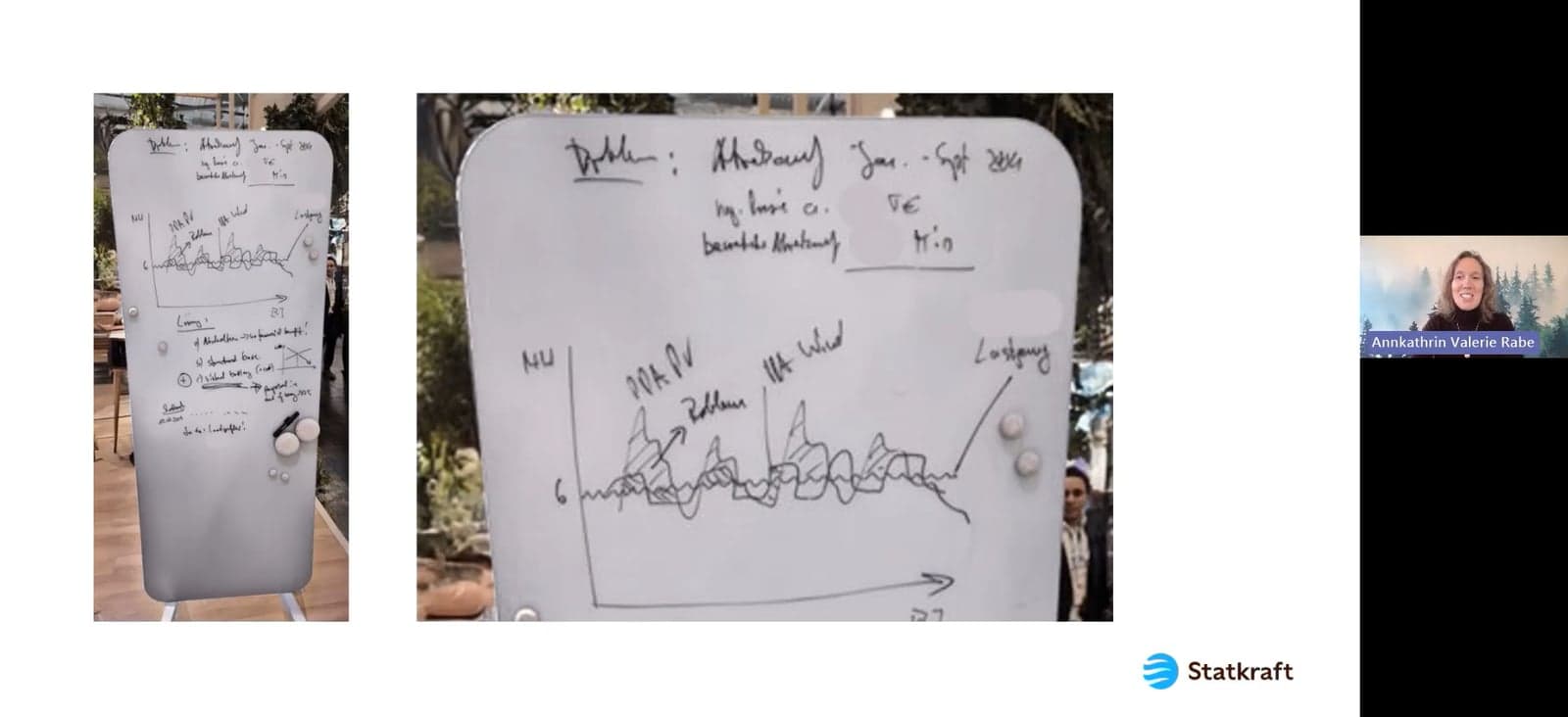

During a webinar hosted by the European renewables company, Annkathrin Valerie Rabe, the company’s Head of Downstream Origination in Germany, shared an example from a PPA customer, which tells the story clearly.

Their demand curve — relatively stable — was layered against wind and solar generation profiles.

Said Rabe: “You can see here on the whiteboard, he was drawing his demand profile, the wavy line you can see in the middle.

“On top, he put his solar and wind profiles. Then he marked the area of oversupply and wrote ‘problem’ next to it. You can see that our customer was facing some issues with oversupply, especially of solar PPAs.”

Three recurring market conditions, explained Rabe, underpin this dynamic.

First, the so-called Dunkelflaute — extended periods of low wind and solar output. During these events, generation under PPAs drops off sharply, forcing buyers into the spot market at precisely the wrong moment. Prices in late 2024 spiked as high as €800–€900/MWh.

Second, the Hellbrise, the opposite extreme: high wind and high solar output. Here, prices collapse. In one July example, average spot prices fell to €43/MWh against a yearly average closer to €80/MWh. For a PPA buyer, excess generation becomes a liability, sold back into a weak market, often at a loss.

Third, the increasingly common “solar-heavy” days, Solarinfarkt: strong midday generation with weaker wind output. These create sharp intraday spreads, with price differences exceeding €200/MWh between the cheapest and most expensive hours.

In the end, we do see that there is a potential increase of all three phenomena, driven primarily by the expansion of renewables.

Said Rabe: “We can see that this price spread between the cheapest and most expensive hour of a day has been increasing over time. We see that on an annual level and a monthly level. If we look at the past two years, 2024 and 2025, we can also see that the number of negative prices is increasing.

“In the end, we do see that there is a potential increase of all three phenomena, driven primarily by the expansion of renewables. We had quite a significant historical build-out of solar in 2024 and 2025 in Germany and very ambitious targets regarding the build-out of more wind and solar. So we expect that the build-out of renewables will increase the effects on spot prices of all three phenomena.”

All of this, of course begs the question of how to balance this all out. And this brings us to batteries.

From flexibility to hedge

The traditional view of BESS is rooted in arbitrage: charge when prices are low, discharge when they are high. That still holds. But the more interesting shift now is how batteries reshape exposure.

Take a typical solar profile. Production peaks at midday — exactly when prices are weakest. Rabe pointed out an example from May 2025, when the average base price was around €64/MWh, but the value of the solar profile was only around €17/MWhhour, about 25% of the base price.

Introduce a four-hour battery, and the profile changes.

Instead of pushing volume into the lowest-priced hours, energy is stored and shifted into the morning and evening peaks. The result is not just higher captured prices, but a different revenue profile.

More from the Power Playbook:

What do falling renewable PPA prices signal about Europe’s energy transition?

Can the EU's Clean Energy Investment Strategy work?

Iberdrola's grids-first strategy pays off early as E.ON and Enel double down

In that same example, the combined solar-plus-storage output achieved a value of €67/MWh — effectively restoring it to parity with the market average.

This is the hedge.

Not against absolute price levels, but against shape risk — the growing disconnect between when energy is generated and when it is most valuable.

It also directly addresses the two key risks emerging in renewable-heavy systems: widening intraday spreads and increasing negative price periods.

Batteries do not eliminate these dynamics. They monetise them.

A market built on spreads

This is where the broader market context becomes important.

Forecasts for emerging storage markets point to the same structural shift.

As discussed by a recent forecast from Aurora Energy Research on Greece’s battery market, wholesale electricity markets are expected to become increasingly polarised between periods of high and low prices. Additionally, says Aurora, Energy arbitrage is likely to be the main revenue source for merchant two-hour standalone BESS entering from 2027, with solar co-location improving returns through stronger day-ahead trading and cost-savings.

At the same time, revenue stacks are becoming more complex. Batteries can participate across day-ahead and intraday markets, balancing services, and ancillary products. But not all of these revenue streams are stable.

Aurora’s analysis adds that risks for the country include limited access to balancing markets, low power prices and overbuild of BESS, showing that restricted balancing access could cut revenues by up to 12%, while faster deployment may further compress returns due to price cannibalisation.

That leaves arbitrage — and by extension, volatility — as the core driver of value. Which is why hedging is moving up the agenda.

Hedging mechanisms will be key to unlocking financing and supporting the next wave of BESS deployment in the Greek market.

Said Aurora's Louiza Moutafi, Research Associate, in a release: "Ensuring bankability is one of the most critical challenges for merchant battery projects in Greece today. As revenue streams evolve, developers and investors must carefully navigate market risks, particularly the increasing cannibalisation in balancing markets.

"At the same time, opportunities are emerging through energy arbitrage and RES-BESS co-location.

"Hedging mechanisms will be key to unlocking financing and supporting the next wave of BESS deployment in the Greek market."

Mechanisms like tolling agreements, day-ahead spread swaps, and hybrid PPAs, says Aurora, can be used to stabilise merchant BESS projects bankability.

These hedging strategies can generate contracted revenues, which can cover material amounts of the project’s lifetime earnings. Similar structures have already enabled BESS financing across European markets, it adds.

Where this leaves the market

The implication is subtle but important.

BESS is increasingly becoming a financial instrument embedded within energy portfolios — one that can absorb volatility, reshape risk exposure, and, under the right conditions, create predictable value streams.

But like any hedge, it is not without limits.

Returns remain sensitive to market design, access to revenue streams, and the pace of deployment. Too much capacity, and arbitrage spreads compress. Too little access to balancing markets, and revenues fall short.

Still, the direction is clear.

As renewable penetration increases and prices become more volatile, the question is no longer whether flexibility is needed.

It is how that flexibility is structured, priced, and ultimately financed.

Batteries, it seems, sit at the centre of that equation as a hedge against the very volatility the energy transition is creating.

But I’m interested to hear about your operations. How have batteries shaped your strategies and impacted your portfolios?

Reach out and let me know so that I can feature your thoughts in the Power Playbook.

Cheers,

Yusuf Latief