IEA flags slow uptake of grid resilience tech

Jonathan Spencer Jones

Posted on: 20 February 2026

Grid operators are facing a range of challenges but there is sluggish uptake of technologies that can address these, the IEA reports.

The new State of Energy Innovation Review from the IEA highlights the range of options across all categories of grid equipment for assuring grid resilience that are already technically proven but face cost, performance and regulatory barriers to their adoption.

Describing electricity systems as “the largest machines operated in the world” – for perspective, laid end to end the world’s powerlines would stretch some 84 million km, more than half way to the sun – the IEA categorises four major technical challenges that are being faced from factors such as rising and changing demand, ageing infrastructure and increased extreme weather and cyber events.

These are ensuring real time stability and power quality, system adequacy and flexibility, physical resilience, and effective grid governance, interoperability and cybersecurity.

Also of interest

Energy innovation funding going through transition says IEA

Mainstream technologies that are still not used in many grids include HVDC systems, static compensators and frequency converters, renewables forecasting tools, synchronous condensers, large-scale stationary batteries, and telecommunications for enhanced monitoring and control at the edges of the grid.

Technologies available to the market for the past decade, but with uptake remaining low, include grid forming inverters, distributed resource energy management systems (DERMS), virtual power plants (VPP), dynamic line rating, and grid digital twins.

There is also a smaller number of early-stage low technology readiness level (TRL) technologies that, with further adaptation, could potentially be successfully transformed into improved products. However, except for certain proposals for long-duration energy storage in novel batteries or thermal or mechanical processes, there are very few entirely new classes of technology at low TRL for which there are still high uncertainties about capabilities.

This group of technologies includes E-STATCOMs, high-temperature superconducting cables, smart transformers, AI-powered grid health monitoring and forecasting, and multi-terminal HVDC networks.

Need for innovation

The report adds that the availability of many technologies at TRL 9 does not mean that technology innovation is not important. A key aspect is that, for electricity grids, their optimisation for system-wide coordination and value is what matters, not just their individual maturity.

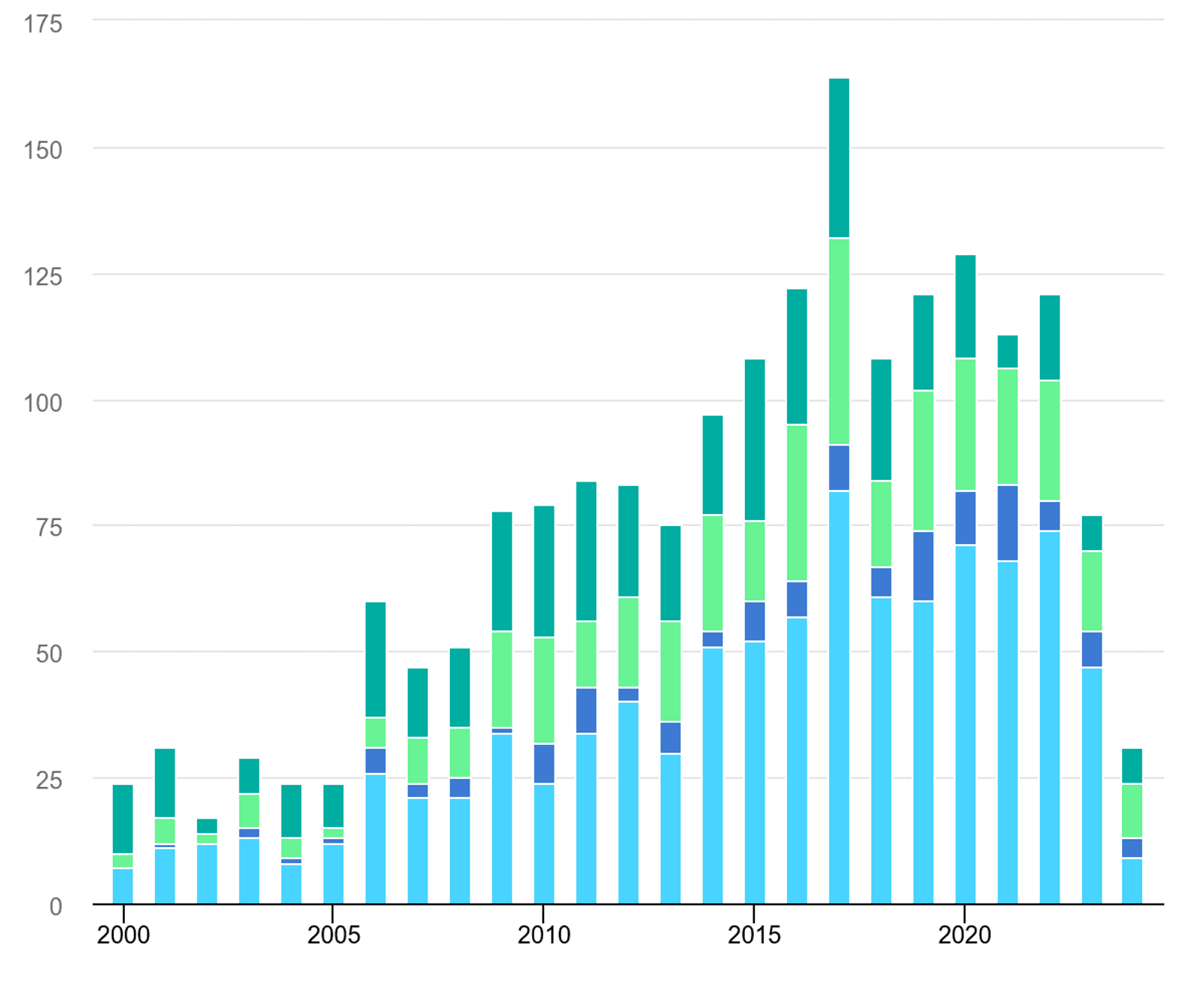

In addition, innovation during the early phases of deployment is still intensive and leads to many startups being founded – around 120 each year since 2016 by entrepreneurs in new grid technology, with many in the area of energy storage and battery developers in particular helping to push up venture capital fundraising to $6billion in 2022.

Despite a decline in funding since then, largely due to the decline in attractiveness of venture capital compared to other investments, it is still seen as an area with dependable growth potential.

Commercialising a high TRL technology also involves innovation but of different types, such as improvements to manufacturing, competition among suppliers with alternative designs and learning-by-doing, which can lead to reduced costs and better product offerings.

This process cannot happen without supportive markets, investors, standards and business models. In the case of electricity grid technologies, regulation and alignment between TSOs and DSOs in different regions is a major factor.

Innovation priorities

For the technologies that are already technically proven in a given context – grid-forming inverters, synchronous condensers, HVDC, advanced conductors and VPPs, long-duration storage, dynamic ratings, self-healing automation, etc. – the next frontier is creating the rules, incentives and infrastructure at a system-wide level for them to operate on complex grids and become routine, the IEA says.

For other emerging technologies and nascent ideas, R&D funding and a clear path-to-market remain crucial.

Specific policy proposals are:

- Raise the incentives for grid operators and resource owners to adopt non-traditional technologies by shifting to paying for outcomes.

- Establish rules and environments such as regulatory sandboxes to demonstrate technical effectiveness in controlled, real-world conditions.

- Develop widely used resilience metrics to evaluate system-level benefits to inform investments, including for pilot projects, and embed them in procurement decisions and regulations.

- Boost R&D, demonstration projects and international cooperation for early-stage and high-cost new technologies with clarity on lifetimes and how costs will decline, so that they can be adopted quickly once their economics improved.

- Develop international standards and protocols for digital controls, forecasting, AI and data exchange and enforce them via grid codes and procurement specifications.