How data centre-driven power demand is shaping big tech power plays

Yusuf Latief

Posted on: 6 March 2026

As Donald Trump lauds his now-signed ratepayer protection pledge, how is the booming power demand from AI and data centres reshaping capital activity for utilities and big tech companies?

In this week's Power Playbook: As AI drives an unprecedented surge in electricity demand, technology companies are increasingly moving beyond simply buying power — and into shaping how it is produced.

That shift is visible in policy, project structures and capital markets activity.

In the US, major tech companies Google, Microsoft, Meta, Oracle, xAI, OpenAI and Amazon have signed US President Donald Trump's Ratepayer Protection Pledge.

Announced last week during Trump's State of the Union address, the pledge obliges these companies to pay for their own power needs, reflecting the mounting pressure that's been placed on power systems as data-centre demand surges, leading to spiking costs for consumers.

Said Trump: "Under this new agreement, big tech companies are committing to fully cover the costs of increased electricity production required for AI data centres...This means that the tech companies and data centres will be able to get the electricity they need all without driving up electricity costs for consumers."

Said Ruth Porat, President and Chief Investment Officer of Google: "I'm pleased to be here to underscore Google's support for the Ratepayer Protection Pledge...We will meaningfully invest across America to bring new energy online...to deliver this self-sufficiency that is core to this pledge."

Behind the politics, however, the announcement is emblematic of a structural shift in how electricity infrastructure is financed and developed around data centre operations.

Data centres as energy platforms

Trump's announcement is the latest in response to how data centres have become some of the most energy-intensive assets in the modern economy.

As a result, their business models are increasingly tied not just to connectivity and computing capacity, but to long-term access to reliable and affordable electricity. And that dynamic is already reshaping deal structures.

Take a new project in Pine Island, Minnesota, where Xcel Energy has signed an agreement to supply power to a new data centre operated by Google.

Under the agreement, Google will cover any new grid infrastructure costs associated with the project.

A Clean Energy Accelerator Charge (CEAC) – a new regulatory tariff developed by Google and Xcel to fund the project - will fund 1,400MW of wind and 200MW of solar, along with a $50 million investment towards Xcel Energy’s Capacity*Connect Program, which will help drive reliability on the grid.

The clean energy resources funded through the agreement also include a 300MW/30GWh Form Energy iron-air battery system installation, the largest battery project by gigawatt-hour energy capacity announced to date in the world.

This 100-hour battery system will store energy during periods of high production and low demand and dispatch it to the grid during times of high demand, providing firm capacity and strengthening grid reliability when it is needed most, even over multiple days.

Commenting in a release was Bria Shea, President of Xcel Energy–Minnesota, North Dakota and South Dakota: “Data centres are the backbone of the 21st century economy, and we’re excited to work with Google to advance the prosperity of our region and ensure our current customers benefit."

This kind of arrangement — where hyperscale technology companies effectively pay for new infrastructure — is increasingly becoming a key feature of the market.

Hyperscalers pulling ahead

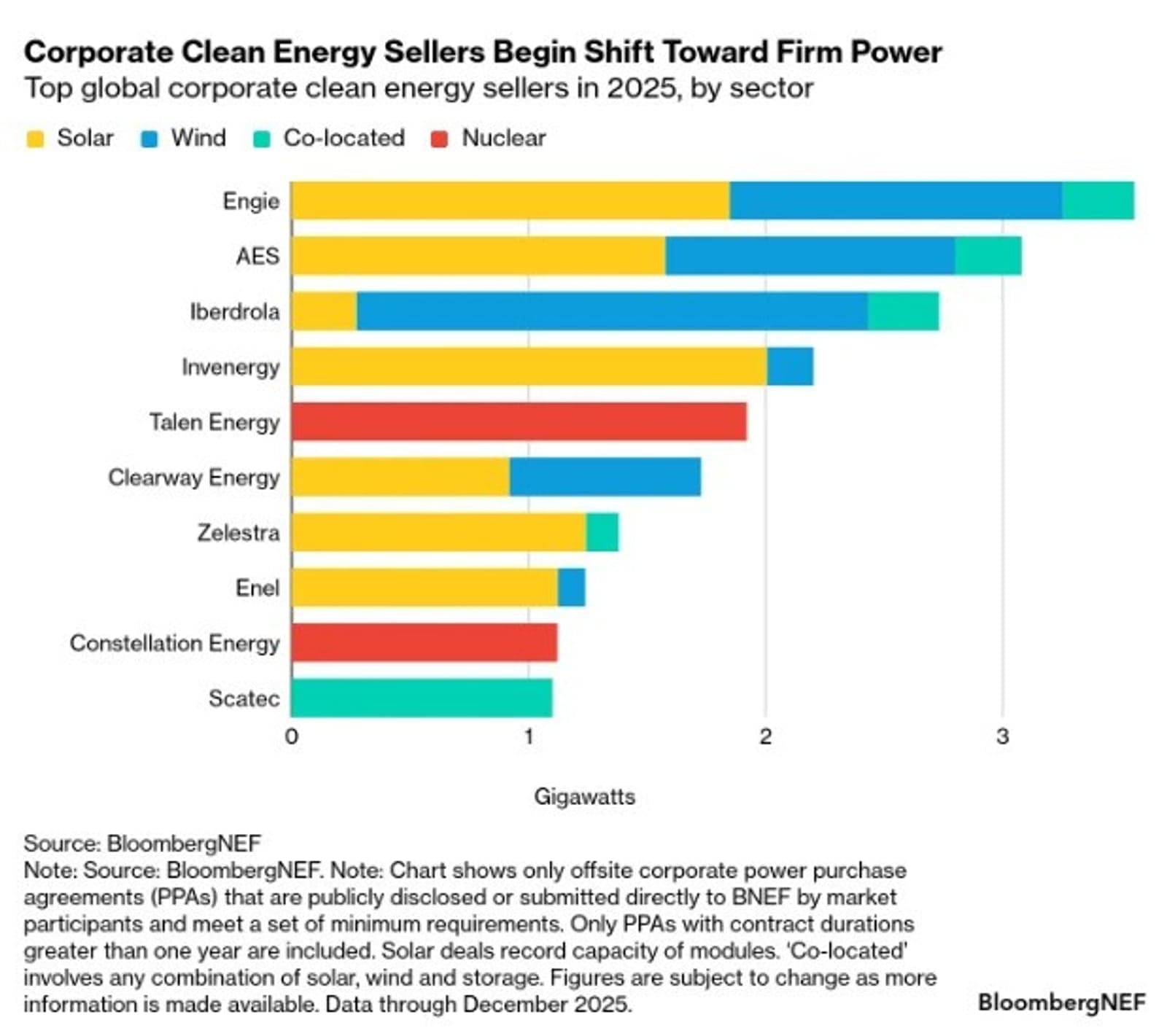

The scale of corporate energy buying highlights just how concentrated this market has become.

According to data from BloombergNEF’s Corporate Energy Market Outlook, corporations announced 55.9GW of clean power deals in 2025.

This figure is down 10% from the previous year, the first decline in nearly a decade.

But what intrigues here is the why: it highlights a widening divide between buyers.

Corporate clean energy buyers are operating at two different speeds.

According to BNEF, the market is increasingly defined by a divergence between hyperscalers and the broader universe of corporate buyers.

According to their data, technology giants Meta, Amazon, Google and Microsoft accounted for 49% of global activity.

As Nayel Brihi, BNEF corporate energy analyst and lead author of the report, explained:

“Corporate clean energy buyers are operating at two different speeds. Large tech buyers are venturing into bigger deals and frontier technologies, while smaller companies are grappling with power market realities.”

That shift is now influencing the strategies of energy companies themselves.

Power suppliers follow the demand

Earlier this week, infrastructure investors led by BlackRock’s Global Infrastructure Partners and EQT agreed to acquire AES Corporation in a deal valued at $33.4 billion.

AES, one of the largest suppliers of clean energy to corporate buyers globally, says the take-private deal will better position it to drive long-term growth across its business units, including regulated electric utilities and competitive clean energy in the US and critical energy infrastructure assets in Latin America.

AES will also have improved access to capital to invest in critical energy infrastructure assets.

With 11.8GW of agreements signed to supply electricity to big tech companies, including Google and Microsoft, AES is no small player.

It is also listed in BNEF’s outlook as one of the top global corporate clean energy sellers in 2025, behind Engie.

And clearly investors have been watching.

Masoud Homayoun, head of EQT Infrastructure, said: “As one of the largest energy infrastructure investors globally, we are seeing first-hand the increasing need for a secure energy supply amid expanding power demand worldwide.

“EQT’s acquisition of AES will support the growth and modernisation of essential energy infrastructure that underpins energy security, electrification, digitalisation and resilient power systems across key markets.”

Demand boom guiding capital flow

Said Andrés Gluski, President and Chief Executive Officer of AES, when commenting on their listing by BNEF:

"We are seeing surging demand for clean energy from the corporate sector, driven in large part by AI data centre development and advanced manufacturing.”

According to Morgan Stanley, this boom in demand and consumption has been accompanied by an increasing appetite from investors for capital markets for methods to finance energy infrastructure quickly.

Investors, they say, have noted that power suppliers and power equipment companies are likely to see benefits from data-centre expansion, particularly given expectations that AI will unleash a productivity wave throughout the broader economy.

This, in turn, has led to investors focusing on rising demand for off-grid solutions, eliminating bottlenecks in the energy supply chain and using credit markets to finance energy system growth.

The result of all this is a new alignment between capital markets and digital infrastructure, where the growth of AI is becoming a driver of energy investment itself.

Europe’s own power race

This trend extends beyond the US. Similar dynamics are also visible across Europe.

In late February, data centre developer Start Campus and EDP announced a partnership to accelerate next-generation, renewable-powered data centre projects in Portugal, with potential expansion to other markets.

Under an MoU, the two will combine their complementary capabilities to accelerate the delivery of competitive, sustainable computational capacity.

The agreement is structured around three core pillars

- Accelerating renewable energy development to support the growing digital demand while enhancing grid resilience and long-term system stability;

- Establishing EDP as Start Campus’ preferred long-term partner for green energy solutions;

- Exploring synergies and angles of cooperation in Sines and in future data centre developments across Portugal and potentially other markets.

The framework is also designed to align new development and investment in the energy and digital sectors across Portugal, initially anchored at the SINES Data Campus.

Additionally, in Amsterdam, hyperscale developer Pure Data Centres in December 2025 launched a data-centre campus already fully leased with power and permits secured.

Situated in Westpoort, Amsterdam, Pure DC will be investing over €1 billion ($1.2 billion) to develop the site.

Chief Executive Dame Dawn Childs said the project reflects the challenge of developing digital infrastructure in constrained energy markets:

“Amsterdam is one of Europe’s most constrained markets for digital infrastructure and Pure DC has again demonstrated its ability to unlock new low-latency, high-quality capacity.”

To secure the project, the company obtained 100MVA of power through a private substation, illustrating just how central electricity access has become to data-centre economics.

More from the Power Playbook:

Iberdrola's grids-first strategy pays off early as E.ON and Enel double down

What do falling renewable PPA prices signal about Europe’s energy transition?

The next phase of the power market

Put these developments together, and a new market structure begins to emerge.

Technology companies are increasingly becoming active participants in the energy system, financing infrastructure and shaping debates about who should pay for the power needed to run AI.

At the same time, the corporate energy market is beginning to split, with hyperscale buyers striking ever larger deals.

It stands to question then what the next decade, and even the upcoming years, will shape up to be for the sector.

If the past decade was about building capacity, the next may be more about who finances and controls this electricity to run the digital economy.

What do you think? How will the dynamics evolve between tech companies and electric utilities as demand only continues to surge?

Reach out so that I can feature your thoughts in the next Power Playbook.

Cheers,

Yusuf Latief

Related tags

Latest in Digitalisation

All articlesPartner content

+1

Digital water management: Empowering utilities with scientific decision-making

As urban water distribution networks continue to expand and water resource management becomes increasingly complex, water utilities are facing growing operational challenges.

- Guest/partner contributor

- 03/07/2026